It’s been well documented that the pain of loss exceeds the joy of gain. It logically follows that most investors would prefer to outperform a benchmark during a bear market (i.e. lose less) than a bull market (i.e. earn less).

Seems intuitive. If markets are up 20% and you earn 15% you’re happy you’re making money. Yeah there’s greed and fear of missing out but profits are profits. On the other hand if markets are down 20% and you’re down 15% you’re not feeling great yet appreciate how much worse it could be.

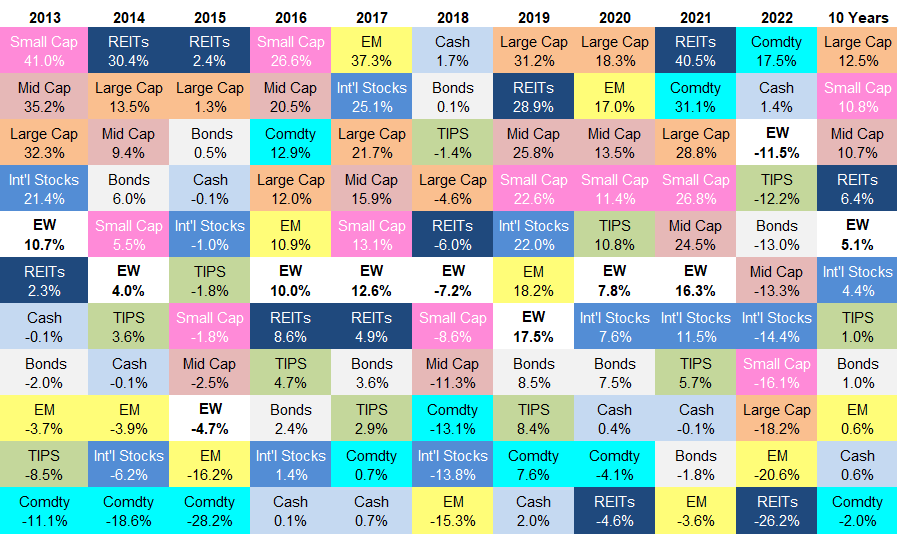

Take a look at asset class return data from 2013-2022:

cash: (SPDR Bloomberg 1-3 Month T-Bill ETF)

TIPS: US government bonds (iShares TIPS Bond ETF)

bonds: (iShares Core US Aggregate Bond ETF)

large cap: (SPDR S&P 500 ETF)

mid cap: (SPDR S&P 400 MidCap ETF)

small cap: (SPDR S&P 600 Small Cap ETF)

int’l stocks: international stocks (iShares MSCI EAFE ETF)

EM: emerging market stocks (iShares MSCI Emerging Markets ETF)

REITs: real estate investment trusts (Vanguard Real Estate Index Fund ETF)

comdty: commodities (Barclays Bank iPath Bloomberg Commodity Index Total Return ETN)

A diversified portfolio (labeled “EW” for an equal weighting of asset classes) almost always lies in the middle. It’s a feature not a bug.

Diversification ensures investors never have the worst performance at the cost of never having the best. Isn’t that what pain avoidance is all about?

There’s an old saying that we can have things fast, cheap and good but can pick only two. Fast and cheap isn’t always good. Investing, however, and the rise of low-cost index products just might violate this rule. Food for thought.

As always there’s no single solution that works for everyone. Our individual circumstances dictate the what, when, why and how.

Data is but one variable. One input. Use it wisely.