A bit more than ten years ago Lehman Brothers which at the time was the 4th largest investment bank in the U.S. filed for bankruptcy protection. The event has become the symbolic start of what’s been called the Global Financial Crisis (“GFC”). Today we continue to see its effects on both the global economy and investor behavior.

A reminder of some of the damage to the US:

- GDP declined by 4.7% from 2008 through the first half of 2009

- over 8,000,000 people lost jobs between 2008 and 2009

- over 8,000,000 people lost homes through foreclosure

- the average home value declined by 32% from the 2006 peak to the 2009 trough

- household net worth declined by $17 trillion from 2007 through the first quarter of 2009

- retirement account values fell by roughly 1/3 from Sep 2007 through Dec 2008

Finger pointing was rampant in the aftermath. Main St occupied Wall St as presumably things were the fault of the banks and the one-percenters. Obama ripped into the educated, high-income white males – those evil millionaires and billionaires. The average American who had no idea Donald Trump would run for POTUS eight years later took to Facebook to blame him. (OK, so we made up that last one. Or did we? It’s on the internet so it must be true, right?)

Economic impact in the years that followed:

Interest rates remained low. The desire for relatively safe assets pushed up the price of bonds and, inversely, lowered their yields. Governments in relatively safe countries such as the US, UK and Germany were all too happy to oversupply the markets to finance deficit spending at such a low cost.

So have wages. During economic recovery companies typically outbid one another for human capital. Slowing global growth (see below) has lessened the need to pay up for talent. What’s more as Baby Boomers retire they are replaced by younger, cheaper workers.

Global growth and international trade has slowed. The developed world pulled back on its debt-fueled consumption. Emerging markets had fewer customers for their goods as growth in these markets shrank from 7% to 4%. China’s trade surplus shrank as it shifted its economy away from exports towards domestic-oriented activities. Its growth rate has slowed from 10% to 6.5%.

Despite the economic impacts financial markets have been strong. US stocks lost 47% of their value from 4q08 through 1q09. They subsequently returned an average annualized return of 19%. Inclusive of the aforementioned loss the average annualized 10-year ROR has been 11%. For comparison it was 9% for the two decades before the GFC.

Investor behavior has become polarized:

Risk-averse investors remained in bed with the covers pulled over their eyes. They panicked, sold at market lows (because action is always better than no action, right?), locked in losses at artificially-low market prices and sat on the sidelines while markets recovered. They refused to play the long game and they got burned.

Risk-loving investors piled into FAANG (Facebook, Amazon, Apple, Netflix and Google). Buying $1,000 of Apple stock in Aug 2008 would grow to $9,200 a decade later. Yet the selloff of the past few months has induced panic. Once again investors fail to see the big picture.

Consistent across the two groups is an increased fear of loss. That’s the one constant and possibly permanent aftereffect of the GFC.

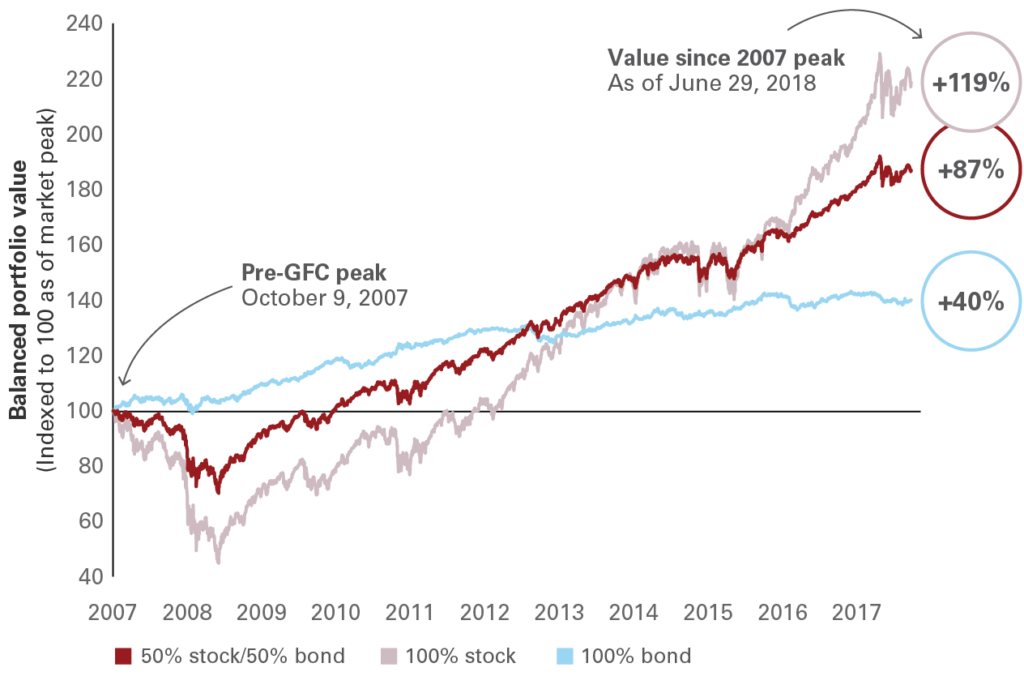

So what about investors who did play the long game? Consider the following:

Investors who did not sell through the GFC but held their entire portfolio in stocks earned 119%. Interestingly enough they were under water the first four years.

An investor holding a 50/50 balance of stocks and bonds earned an 87% ROR.

Even risk-averse investors holding a 100% bond portfolio took in a respectable 40%.

The takeaway is simple and quite timely given the current market volatility. Find a level of risk with which you’re comfortable, build a diversified portfolio within that asset allocation and rebalance from time to time. That means adding stocks when prices fall and pruning gains when markets rise.